Today, more or less everything is digital – and that even includes conventionally analog fields, such as finance. A few decades ago, the traditional finance field looked more or less like it had always done. However, innovations in technology, payment processors, and applications have now made it possible for centralized finance (CeFi) and decentralized finance (DeFi) solutions to offer the same services historically offered within traditional finance. Sometimes it can be challenging to get your head around the differences between CeFi vs DeFi, and how these differ from traditional finance (sometimes known as TradFi). However, fear not – we are here to help explain traditional finance and CeFi vs DeFi!

In this article, we’ve broken down these three common forms of financial infrastructure. Furthermore, we discuss the pros and cons of each while looking at the many crossovers that occur between them. We explore how CeFi vs DeFi applications may not be competing but complementing each other within the space.

If you’re new to crypto, it can be a little overwhelming at times. With so much information available, it’s often difficult to know where to start. However, Ivan on Tech Academy is the best place to start your crypto education. Learn about the history of money and currency with our Bitcoin Standard course. Or, if you want to gain foundational knowledge about crypto and blockchain, check out our Crypto Basics course, available at Ivan on Tech Academy!

What is Traditional Finance (TradFi)?

The term “TradFi” is short for traditional finance, and essentially relates to conventional banks. It all began in 1694 when the Bank of England was founded to look after the gold of businessmen traveling to the country. Carrying gold around was inconvenient and exposed individuals to the vulnerability of being attacked or mugged. It made a lot of sense to businessmen to be able to store their wealth in a secure vault whilst they carried out their business. Businessmen were given a receipt for their gold, which allowed them to redeem their precious metals upon exiting the country.

Additionally, the bank realized that they could profit from the amount of gold passing through their vaults. If businessmen were not returning to claim for their gold for some time, the bank would lend out their gold, in return for an interest rate on their deposit. As this was a form of passive income for the businessmen, it made a lot of sense for them to be ok with the bank doing this.

Over time, it became easier for businessmen to carry out exchanges with the receipts for their gold, than with the actual gold itself. The bank-distributed paper allowed the recipient to claim the amount of gold stated on the receipt. This was the beginning of gold-backed paper currency, distributed in correlation to the amount of gold a government is holding. However, history has repeatedly shown that this financial infrastructure has led to greed and deceit, by debasing the value of a nations’ currency. This happens when the amount of paper printed accounts for more than the amount of gold stored.

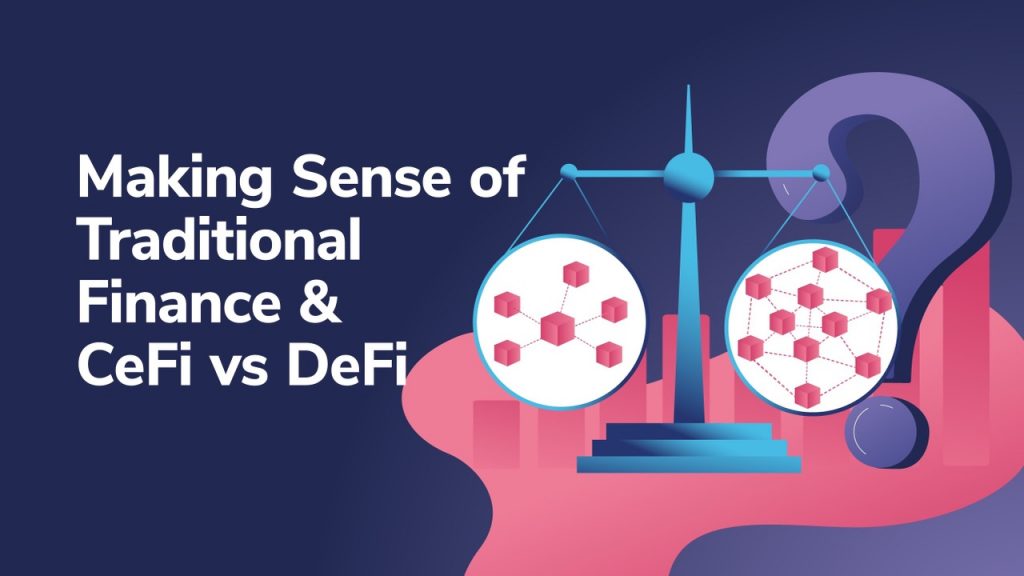

Why Money Changed Forever in 1971

When many countries realized this was the case for the US dollar, they started to demand their gold back. Unable to fulfill requests of these demands, in 1971 President Nixon famously unpegged the backing of the US dollar to gold.

The debt ceiling was removed and the government could print as much money as they liked. Each time, devaluing the currency. Debt, of course, must be repaid, which can only be done through inflationary and tax measures. Therefore the average person pays more for their goods, with the paper money that continues to be worth less each day. If you would like to read more about how you can make your ‘money’ go further, save our Bitcoin vs Stocks vs Gold article for later!

Pros & Cons of Traditional Finance (TradFi)

Pros:

- Most people use traditional finance (TradFi) as it’s currently the largest, most familiar financial infrastructure.

- TradFi has evolved slowly over the decades and has a documented history.

Cons:

- Funds in your account are loaned out, your bank balance is essentially an IOU from the bank.

- Unnecessarily expensive transactions.

- Slow transaction times.

- Inflationary currencies.

- Banks are free to implement negative interest rates, meaning customers start paying the bank to hold their funds.

- Requires consistent know your customer (KYC) documentation for sending large transactions.

What is CeFi?

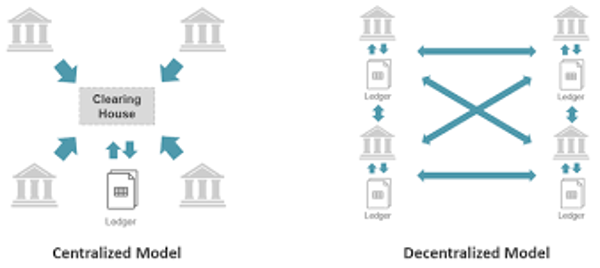

Centralized finance (CeFi) generally refers to financial applications that bridge the gap between traditional finance (TradFi) and modern financial applications. Moreover, centralized finance tends to have a centralized, governing body in control of any funds. CeFi is an umbrella term that is applied to centralized crypto exchanges and custodians, though it could be argued that other payments providers and FinTech applications also fall into this category.

Often, CeFi applications offer custody of funds in a familiar, easy-to-use application. There is a great deal of cross-over between recent innovations in payment technologies. For example, both PayPal and Coinbase could constitute as CeFi as they both offer fiat-gateways to payments services alongside crypto custodial services.

Crucially, when it comes to centralized crypto exchanges and services such as Coinbase or Binance, users do not have to look after their own seed phrases and private keys. This eliminates some of the risks that are inherent with self-custody in crypto and DeFi.

Usually, when a person enters the crypto space for the first time they tend to do it through a centralized exchange (CEX). CEXs provide fiat on-ramps that make buying, trading, and hodling crypto simple.

CeFi applications generally require users to complete know your customer (KYC) and anti-money-laundering (AML) processes. This means providing personal information that ties an account directly to a specific user.

Centralized crypto exchanges (CEXs) are owned by a business or a company. Soon we can expect a Coinbase initial public offering (IPO) as the world’s most popular CEX is to be listed on the stock market. This will allow investors to gain indirect exposure to cryptocurrencies through a regular brokerage account.

Furthermore, CeFi attempts to bridge the gap between decentralized finance (DeFi) and traditional finance (TradFi). As such, most CEXs have high levels of regulation in place.

Pros & Cons of CeFi

Pros:

- Fiat gateway.

- Simple to use.

- No risk of losing private keys.

- Highly regulated.

- Great for onboarding new users.

- Tried and tested.

- Exposure to a wide range of crypto assets.

- Lower trading fees for smaller trades.

- Reputable CEXs usually carry out extensive due diligence before listing a coin, which is reassuring to investors.

- Acceptance from the wider financial community.

Cons:

- Single-point-of-failure. If a CEO or keyholder goes missing, funds could be locked and withdrawals suspended without notice.

- Users do not physically own their crypto assets (not your keys, not your coins!).

- Businesses have investors to keep happy.

- Some CEXs make a mark-up on trades, meaning you pay slightly more than the market price.

- Many CEXs are coming under increasing regulatory scrutiny.

If you’re new to crypto and want to learn more about the wondrous world of DeFi, check out the Ethereum 101 and DeFi 101 courses at Ivan on Tech Academy. Here, you can find all the relevant information you need to get ahead in the world of DeFi. Ivan on Tech Academy is the number one online blockchain educational suite. Regardless of your current level of experience, Ivan on Tech Academy is designed to help you through every step of your journey in crypto!

What is DeFi?

DeFi, short for decentralized finance, is the latest step in the financial technological revolution. DeFi is powered by blockchain technology, and essentially runs on a global network of nodes. These nodes can mathematically verify transactions and record them on the blockchain.

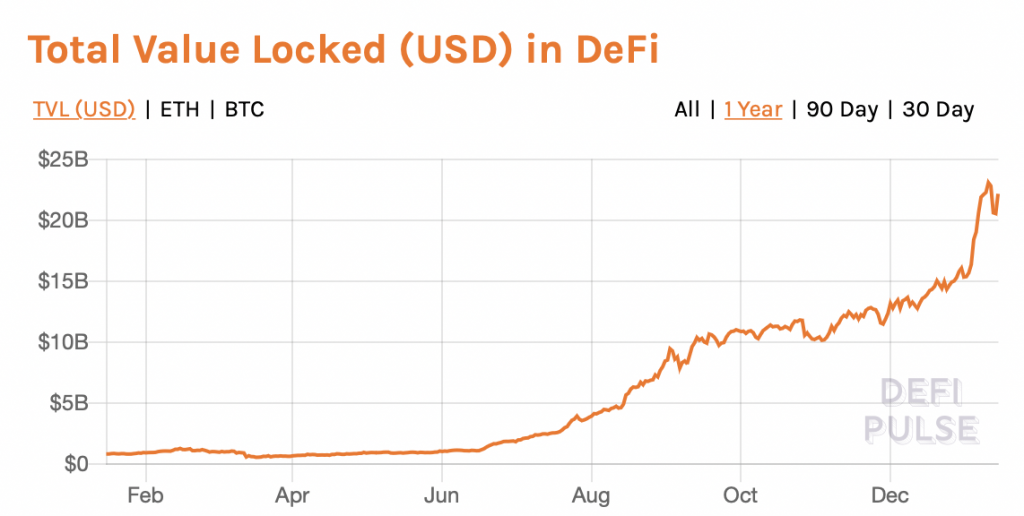

Since 2015, with the introduction of Ethereum, developers have been able to build decentralized applications using smart contracts on top of blockchains. In 2020, we saw an unprecedented amount of growth in the total value locked in DeFi. From around $690 million in January to $16 billion by year’s end. This was expedited by the pandemic, and people recognizing a need to be in complete control of their own wealth.

As decentralized applications (dApps) are built on top of blockchains, there is no single-point-of-failure nor control by a third party or intermediary. Moreover, it means that users of decentralized platforms will need to have custody and access to their funds. This being said, many DeFi applications now have their own wallet built within a decentralized application (dApp). Often, holding a platform’s native token within the dApp wallet entitles users to bonus rewards or perks.

DeFi refers to every decentralized aspect of finance. From DeFi tokens themselves to borrowing and lending, to staking, flash loans, and stablecoins. Even in today’s modern world, approximately 1 in 3 people are unbanked. Furthermore, around two-thirds of this group have access to a smartphone and the internet. This means that millions and millions of people, for the first time, will have access to financial tools and instruments all from their handheld devices. DeFi can help struggling economies, and protect people from their local inflationary currencies.

DeFi has come a long way in a very short space of time. Throughout 2020 we saw the emergence of new DeFi applications, yield farming, stablecoins, decentralized exchanges (DEXs), and marketplaces.

Pros & Cons of DeFi

Pros:

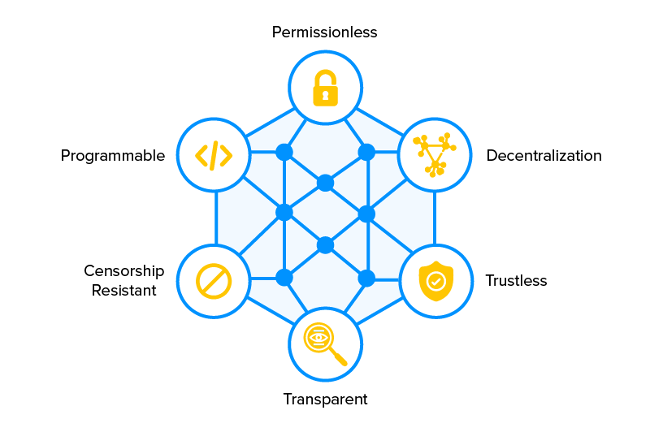

- Censorship-resistant and permissionless promoting financial inclusion.

- Faster, borderless operations 24/7/365.

- Cheaper transactions than TradFi.

- Stablecoins act as a hedge against local currency debasement.

- High yields.

- Young industry – many opportunities.

- Less regulatory scrutiny than CeFi or traditional finance (TradFi).

Cons:

- Can be complicated.

- Responsibility of own private keys.

- Higher risk.

- No customer service.

- Lack of regulation can be a deterrent and hinder adoption.

- Relatively high Ethereum gas fees.

CeFi vs DeFi & TradFi

The world of finance, money, and currency have seen many epochs and iterations. Similarly, people’s methods of exchange have changed from trading shells, rice, and animal hides, to precious metals. Fast forward a few hundred years, and we have moved to gold receipts and fractional reserve banking. Shortly after, fiat currency takes precedence as the dollar loses its gold backing. Then, along comes the internet.

The internet has changed a lot of things, from how we interact with each other to how we learn and how we develop. The finance industry is no exception. The internet revolutionized finance, and most importantly, allowed crypto to come into existence.

Some refer to crypto as “the internet of money”. DeFi and other smart contract-based platforms have allowed for programmable money that is censorship-resistant and free from governmental controls. Despite the comfort and familiarity afforded by the legacy financial system, there’s no doubt that crypto platforms are beginning to catch the hearts of tech-savvy investors from all walks of life. TradFi appears to no longer offer any compelling reason to participate.

Ultimately, when breaking down your choices between CeFi vs DeFi applications, it comes down to the individual. From one perspective, one may look at CeFi vs DeFi applications as competing. However, it has become clear there are benefits, drawbacks, and a need for both CeFi and DeFi platforms and applications within the space.

CeFi vs DeFi & TradFi Summary

In summary, when comparing CeFi vs Defi, you may notice many parallels. For example, Coinbase has investors that want to see returns, as does “decentralized” exchange Uniswap. You can earn yield from CeFi applications that function in a very similar way to DeFi applications.

To many, decentralization is an ideology. Bitcoin rose to prominence in part because it provided an alternative to the traditional financial system. However, decentralized finance is not completely decentralized. Perhaps, a more apt term would be “open finance”. Wrapped Bitcoin (WBTC) is the most popular wrapping service for Bitcoin in DeFi. But, after all, WBTC – for example – is an intermediary in itself.

The other main distinctions to make are custody of assets and anonymity. For example, in some jurisdictions, Coinbase will pass your personal details to the taxman if you make deposits over a certain threshold. The danger of CeFi intertwining too much with traditional finance is that an increase in regulatory pressure threatens the underlying philosophy of cryptocurrencies.

However, many believe that this is an essential part of mass adoption for crypto in the long run. Moreover, as blockchain becomes increasingly utilized by traditional financial institutions, these lines will likely continue to blur.

If you’d like to take your DeFi game to the next level, be sure to check out the DeFi 201 course at Ivan on Tech Academy. Also, if you’d like to learn how to create and automate your trading strategies, take a look at our Algorithmic Trading Course at Ivan on Tech Academy. The world of crypto is changing rapidly. Ivan on Tech Academy brings you all the latest insights into every aspect of blockchain and cryptocurrency, with courses created by our team of industry-leading professionals.