Blockchain is on the lips of everyone, from individuals to institutions these days. Analysts are calling the advent of blockchain (together with other cutting-edge technologies such as artificial intelligence, internet of things and virtual reality) the fourth industrial revolution. However, exactly what is blockchain? This article breaks it all down in a comprehensive “what is the blockchain 101” report.

Blockchain and cryptocurrencies

Blockchain is perhaps most well-known as the technology that underpins Bitcoin and other cryptocurrencies. One should note that blockchain technology has wide-reaching applications that extend far beyond cryptocurrencies. However, the advent of Bitcoin and other cryptocurrencies did help blockchain technology gain more widespread exposure.

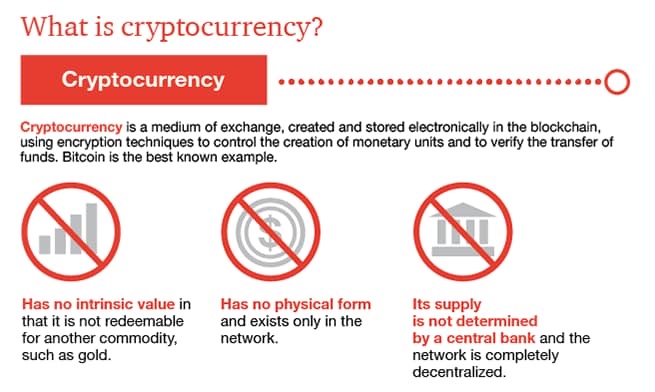

All of these different terms can be somewhat confusing, so we’re going to break it down. Cryptocurrencies are a type of medium of exchange, or means of payment. As such, cryptocurrencies are similar to “fiat currencies” – currencies from central banks, such as the US dollar.

However, unlike fiat currencies which are primarily seen as bills or coins, a cryptocurrency is a digital, or virtual, currency. Moreover, the general idea regarding cryptocurrencies is that they should be immune to manipulation by institutions such as central banks.

Image Source: PWC

As such, there is no central institution in charge of printing and distributing cryptocurrencies. Instead, cryptocurrencies use encryption techniques to control its creation – i.e. “crypto mining” – and to verify fund transfers.

What is a blockchain?

Cryptocurrencies rely on blockchain technology in order to verify these fund transfers and their creation. What, then, is a blockchain? A blockchain underpins every true cryptocurrency, and is a form of a decentralized ledger.

As such, this ledger can keep track of all transactions that happen on the blockchain, or through using the blockchain. The blockchain links an ever-growing number of blocks with cryptography, and these blocks hold records. Every block carries a cryptographic “hash” of the previous block, which proves that the chain of blocks remains unbroken.

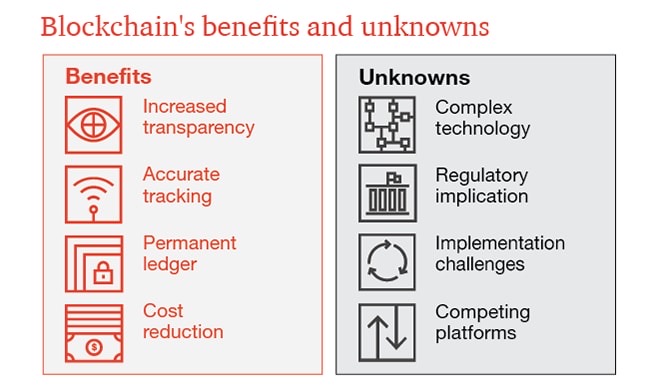

What’s more, this allows participants to confirm transactions without having to rely on a central authority, such as a bank. This allows for a dramatic increase in transparency for the users of the cryptocurrency in question. It also makes it substantially easier to transfer funds across borders or large distances.

Image Source: PWC

There are two main types of blockchains. The first of these is “public blockchains”, which is the blockchains we are most familiar with. The other is “private blockchains”, also known as “permissioned blockchains”, and these are not open to everyone.

Moreover, storing information on a blockchain ledger is permanent, meaning that it is impossible to alter the transaction information afterward. Furthermore, the fact that the network is “decentralized”, i.e. not relying on a single actor, makes it more resilient.

Blockchain and Bitcoin

This, then, leads us to Bitcoin. Bitcoin is the most popular cryptocurrency, or type of digital currency that uses a blockchain. Anyone keeping an eye on the news will know that Bitcoin is all the rage following its astronomic price gains in late $20,000.

Just to recap, 2017 saw the price of Bitcoin explode from roughly $900 at the start of the year to $20,000 in December. This incredible increase in the valuation of Bitcoin also spread to the rest of the cryptocurrency market, which saw large overall gains.

Nevertheless, this price rally was also blockchain technology’s rise to fame. After the very public crypto rally of 2017, companies began taking notice of the underlying technology that was revolutionizing international payments.

As such, numerous companies are now looking to integrate blockchain technology into their businesses. With that said, it is important to keep in mind that blockchain and Bitcoin are separate. However, they both share the same mysterious founder: Satoshi Nakamoto.

Satoshi Nakamoto

The idea of a blockchain, or a “cryptographically secured chain of blocks”, was described by researchers in the early nineties. However, the first known blockchain to actually be built came about in 2008.

Furthermore, this original blockchain was the brainchild of “Satoshi Nakamoto” – who was either a person, a group or an organization. Adding to the mystery surrounding the blockchain and the inception of Bitcoin, nobody knows the true identity of Satoshi Nakamoto.

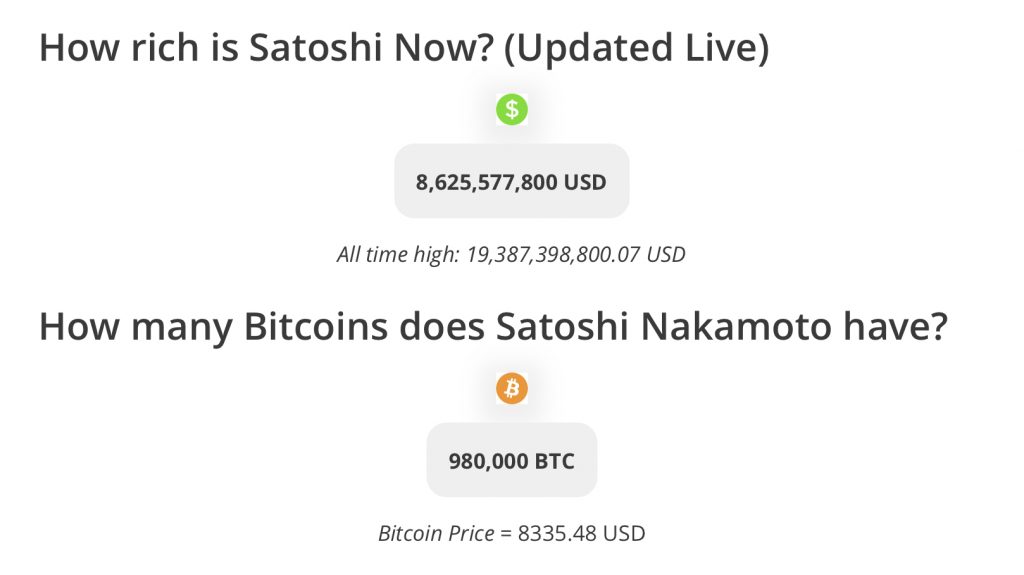

Nakamoto began his work on the code underpinning Bitcoin as early as 2007. However, it took Nakamoto until 2009 to mine the “genesis block of Bitcoin”, or Bitcoin’s block number 0. Notably, Nakamoto’s identity remains unknown until this day – and Nakamoto’s Bitcoin fortune of nearly $9 billion remains unspent.

Image Source: CoinDiligent

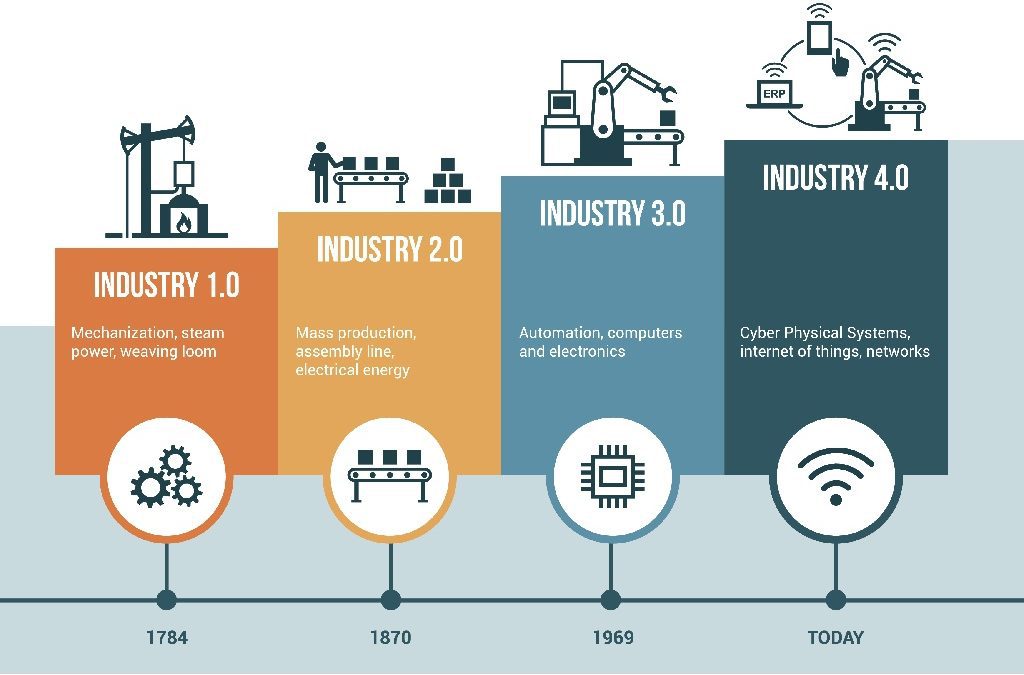

The Fourth Industrial Revolution

Although Bitcoin and cryptocurrencies are interesting on their own, however, blockchain technology is another ballgame. In fact, blockchain technology can do what it did to the payments industry through cryptocurrencies to virtually any industry.

This is because the fundamental advantages of blockchain technology are undeniable and as valuable in logistics as they are to payments. Observers are already suggesting that blockchain technology could play a crucial part in bringing about the “fourth industrial revolution”.

So, what is the blockchain’s role in this new industry? Answering “what is blockchain good for” is relatively complex, seeing as blockchain technology can be so versatile. The true answer is that the blockchain can improve processes for everything from transportation to healthcare.

Describing a blockchain as simply a “digital ledger” does it somewhat of a disservice. To demonstrate the true usefulness of a blockchain, we’re going to go over some concrete use-cases. Now that you know the answer to “what is a blockchain”, you will be able to see the various benefits.

Innovation basically comes in the form of either “vertical innovation” or “horizontal innovation”. Vertical innovation, although radical, primarily impacts a single industry. For example, this could be seen with the discovery of penicillin, the invention of the electric guitar or turbo-charged internal combustion engines.

Horizontal innovation, on the other hand, impacts a broad variety of industries. For example, this includes the invention of the Internet, electricity, or even mastering fire.

What is blockchain in healthcare?

The healthcare sector is still on top of everyone’s minds, following the outbreak of the disastrous COVID-19 coronavirus pandemic. As such, it has become clear for many that health systems around the world are under tremendous strain. Blockchain could ease much of the administrative burden that keeps healthcare workers from focusing on patients.

In particular, the healthcare sector is facing massive data challenges. Moreover, it faces enormous challenges due to data breaches, IT and operations costs, as well as support functions, personnel costs, and insurance fraud.

In addition to being time-consuming, these also represent unnecessary costs the healthcare industry could reduce by implementing blockchain technology.

This could help eliminate the astronomical amount spent globally on healthcare every year. Even before the COVID-19 coronavirus pandemic, global annual health spending was tracking to exceed $8.73 trillion in 2020.

Image Source: OutSquare MD

Most hospitals are still hopelessly analog in the way they keep records. They mainly use paper to record information regarding patients, and store it in physical file cabinets. Although some hospitals have begun pushing for electronic record-keeping systems, these are often incompatible with other hospitals’ systems.

Additionally, there is currently not even a universal system for identifying patients.There is also a trust issue that relates to healthcare records. Employing blockchain technology in the healthcare sector could solve this, and help build trust among patients, consumers and healthcare institutions.

Specifically, blockchain technology in the healthcare sector could allow doctors to easily and securely access patient information. Furthermore, this would be even safer than the way healthcare institutions store medical records today.

Blockchain in transportation

Another sector that could massively benefit from the introduction of blockchain technology is that of transportation. In fact, various transport companies around the world are already beginning to implement blockchain technology in their operations. So, what is a blockchain in the transportation sector and what is it good for?

The transportation industry relies on a massive amount of paperwork. In today’s globalized world, it is exceedingly common to send something across national boundaries. Furthermore, consumers expect these shipments to be quick and without error.

Today, most transportation companies rely on physical ledgers to keep records of shipments. However, blockchain technology could replace these with a single universal tracking system for transport. Moreover, this could be far superior to existing tracking techniques.

Image Source: Bitnewstoday

For example, smart contracts could simplify customs clearance and checkpoints, and make sure they happen without any errors. Furthermore, one could integrate traffic sensors and tracking to follow the package in real-time. Naturally, blockchain technology could also dramatically reduce the necessary amount of administration work for transportation duties.

The transportation and shipping industry is only going to keep growing in importance in the years to come. Moreover, blockchain technology could revolutionize it by boosting accountability, traceability and transparency.

In fact, integrating blockchain solutions in the transportation sector is long overdue. This could lead to faster deliveries, quicker resolution of disputes, cut down processing costs and time. Additionally, it could also allow for back-tracking in the supply chain, using the digital ledger.

What is a blockchain in the real estate sector?

Those working in real estate would likely have a different answer to what a blockchain could and should be. It is well-known that the real estate industry is a hectic business, that relies heavily on paperwork and documentation.

Much like in the healthcare and transportation sector, this is something the real estate sector could alleviate with blockchain technology. In fact, selling and buying homes “on the blockchain” has the potential to transform the process of real estate dramatically.

First and foremost, storing all information about houses in a digital ledger – i.e. a blockchain – could boost transparency. This could provide tenants, real estate agents and prospective buyers with an immutable “master ledger” with all the information regarding a building.

This could, for example, include various documents, as well as information on past house prices, construction work done at the house, or other notable information about the building. As such, this information could be readily available.

What’s more, a real estate blockchain application could even allow seller and buyers to have direct contact. This could eliminate middlemen and high commission rates. For the ultimate blockchain experience, the purchase could happen with a smart contract – which releases funds only when conditions are satisfied – and paid in cryptocurrency.

What is the blockchain in the restaurant industry?

Our last example examines applications for blockchain technology in a wholly separate sector from the previous ones – the restaurant industry. The restaurant industry is consumer-facing and already deals with a lot of data.

A restaurant blockchain could help locations keep track of numerous transactions in real-time. This would not only speed up payments, it could also provide restaurants with a comprehensive ledger of purchases and sales.

Moreover, the blockchain can help restaurants trace groceries and food from suppliers. As such, it is possible for restaurants to immediately receive a notification if there is something wrong with a shipment of food supplies.

Consequently, the restaurant can dispose of the affected groceries in a cost and time effective manner. This is in stark contrast to the current situation, where suppliers sometimes have to issue nationwide recalls to avoid food safety disasters.

Furthermore, a blockchain could allow farmers to directly present end-buyers with relevant data regarding their commodities. This means restaurants can easily purchase supplies directly from the farmers, without needing a middleman.

Real-world blockchain summary

As this breakdown gives explains what the blockchain is and demonstrates how various industries could benefit from it, it seems clear blockchain adoption is on the rise. Moreover, the aforementioned examples only begin to scratch the surface of what the blockchain is and what the blockchain can be.

Consequently, virtually anyone is able to take advantage of blockchain technology in their own business. One great example of this is the Ivan on Tech Academy Blockchain Business Masterclass. What are you waiting for?