In this article, we dive deep into the rumors of a USD Coin (USDC) collapse and evaluate the credibility of the claims. Also, we consider the future of stablecoins and the increasing need to develop legislative and regulatory frameworks. Firstly, we explore the basics of stablecoins, including the different types available.

For a deeper understanding of how this cutting-edge technology works, see our Blockchain & Bitcoin Fundamentals course at Moralis Academy! Or, to learn about the differences between leading projects, check out the free Moralis Blog! For example, why not save our “Solana vs. NEAR” article or our “Rust & Solana” article for later?

What are Stablecoins?

Fundamentally, stablecoins are a form of cryptographic asset that maintain a stable price pegged to the value of another asset. Typically, stablecoins are pegged to the value of one US dollar. However, other stablecoins can hold a price value equivalent to commodities or local currencies (e.g., gold, AUD, EUR, etc.). Stablecoins allow traders and investors to hold their wealth in a stable-priced asset, maintaining an investment value during market volatility. The stablecoin ecosystem represents a $153 billion market capitalization, according to CoinGecko, of an overall $900 billion crypto market cap at the time of writing. Moreover, the stablecoin industry has seen a nearly 3,000% increase since 2020.

Despite substantial growth, the stablecoin ecosystem is seemingly on shaky grounds with the recent collapse of the stablecoin project, TerraUSD. Additionally, leading stablecoin projects Tether (USDT) and USD Coin (USDC) have come under scrutiny regarding the validity of their underlying assets and regulatory compliances. To understand why the future of stablecoins appears so uncertain, you must first understand the different types of stablecoins and how they work.

Different Types of Stablecoins

We can break down the different types of stablecoins into the following categories: custodial (or centralized), non-custodial (or decentralized), collateralized, and non-collateralized. Custodial stablecoins are akin to using poker chips in a casino. Each poker chip, or stablecoin, is redeemable at a constant 1:1 ratio in US dollars. Plus, holding poker chips allows you to participate in a gaming ecosystem unavailable to cash holders. Similar to exchanging poker chips for dollars with a cashier, users can exchange their stablecoin assets for US dollars using a crypto exchange. In order for the above economic mechanism to function, each poker chip must be fully backed by dollars. This is to ensure that players can receive their equivalent US dollar value in the event everyone returns all their poker chips at once.

Thus, custodial stablecoins are assets under the authority of a governing custodian, allowing investors price exposure to stable-value cryptos. Moreover, each stablecoin is fully-collateralized with off-chain assets. Often, this takes the form of fiat currency reserves or physical commodities. However, the custodian of the underlying stablecoin asset may choose to use an idle reserve of funds to make a passive income by investing in highly liquid assets. For example, this could include treasuries or short-term commercial debt. Alternatively, funds could be placed into an interest-bearing account.

Users of centralized or custodial stablecoins are often unaware of the underlying financial operations of the stablecoin issuer. Furthermore, there is currently no legal obligation for stablecoin providers to be fully transparent with users regarding their financial activities. This being said, it is a legal obligation for custodial stablecoin issuers to provide annual proof of ownership for their underlying assets to the local authorities.

Non-Custodial (or Decentralized) Stablecoins

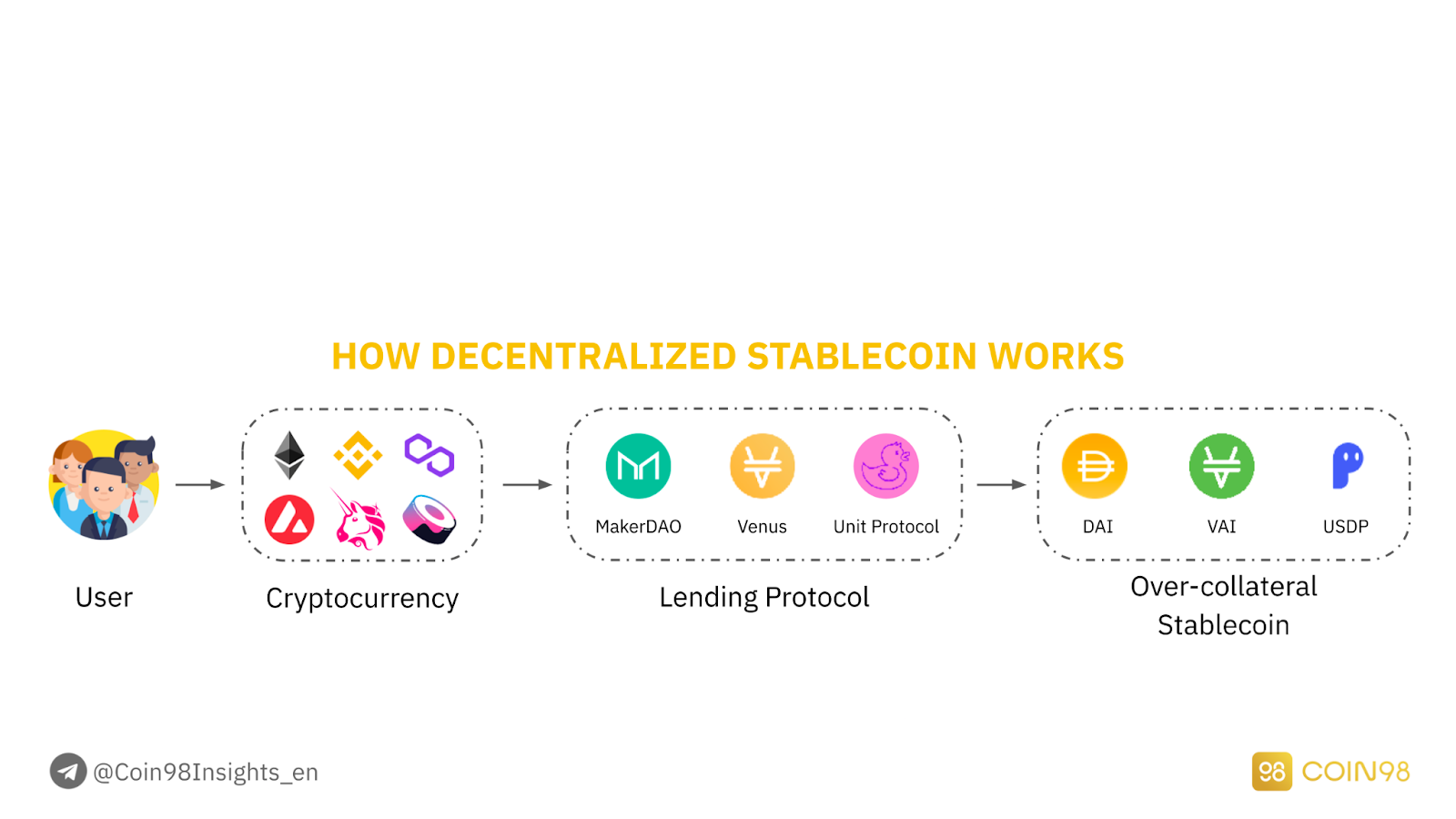

On the other hand, non-custodial or decentralized stablecoins are a cryptocurrency design that maintains the price stability of an underlying asset but without the need for a governing custodial service. As such, non-custodial stablecoins fundamentally operate as pieces of code or smart contracts.

Plus, in conjunction with the hosting blockchain’s consensus mechanism, a non-custodial stablecoin platform will operate with an incentive-based economic design to maintain the stablecoin’s price stability. Overall, non-custodial stablecoins provide a decentralized alternative to custodial stablecoins, with two primary options. Non-custodial stablecoins can either be collateralized or uncollateralized (or “algorithmic”). This being said, some stablecoin projects use a hybrid approach (i.e., partially collateralized). But, some of the most commonly-used stablecoins in the decentralized finance (DeFi) industry fall into one of the following categories.

Collateralized Non-Custodial Stablecoins:

Unlike the collateral underlying custodial stablecoins, collateralized non-custodial stablecoins typically use other cryptocurrency assets, i.e., ETH. As a result, with far higher risks of volatility compared to the underlying assets of its custodial counterpart, non-custodial stablecoins often require over-collateralization. Instead of users exchanging funds using a centralized exchange, users can deposit their assets into a smart contract and receive decentralized stablecoins in return.

However, unlike custodial exchanges that offer a 1:1 exchange of assets (potentially minus a small transaction fee), non-custodial collateralized stablecoins require users to deposit collateral of a higher value than the stablecoins they receive. For example, users may deposit $1.50 or $2 worth of ETH into a smart contract and receive $1 worth of stablecoin in return. The stablecoin is then fully redeemable 1:1 for the dollar value in ETH upon depositing the stablecoin back into the contract.

Each stablecoin protocol will have its own parameters around collateralization and liquidation thresholds. Smart contracts are programmed to automatically liquidate the underlying collateral should the price of ETH fall below the set threshold. Theoretically, this ensures a continual sufficient amount of underlying assets to be redeemable for all stablecoins in circulation.

Uncollateralized Non-Custodial Stablecoins

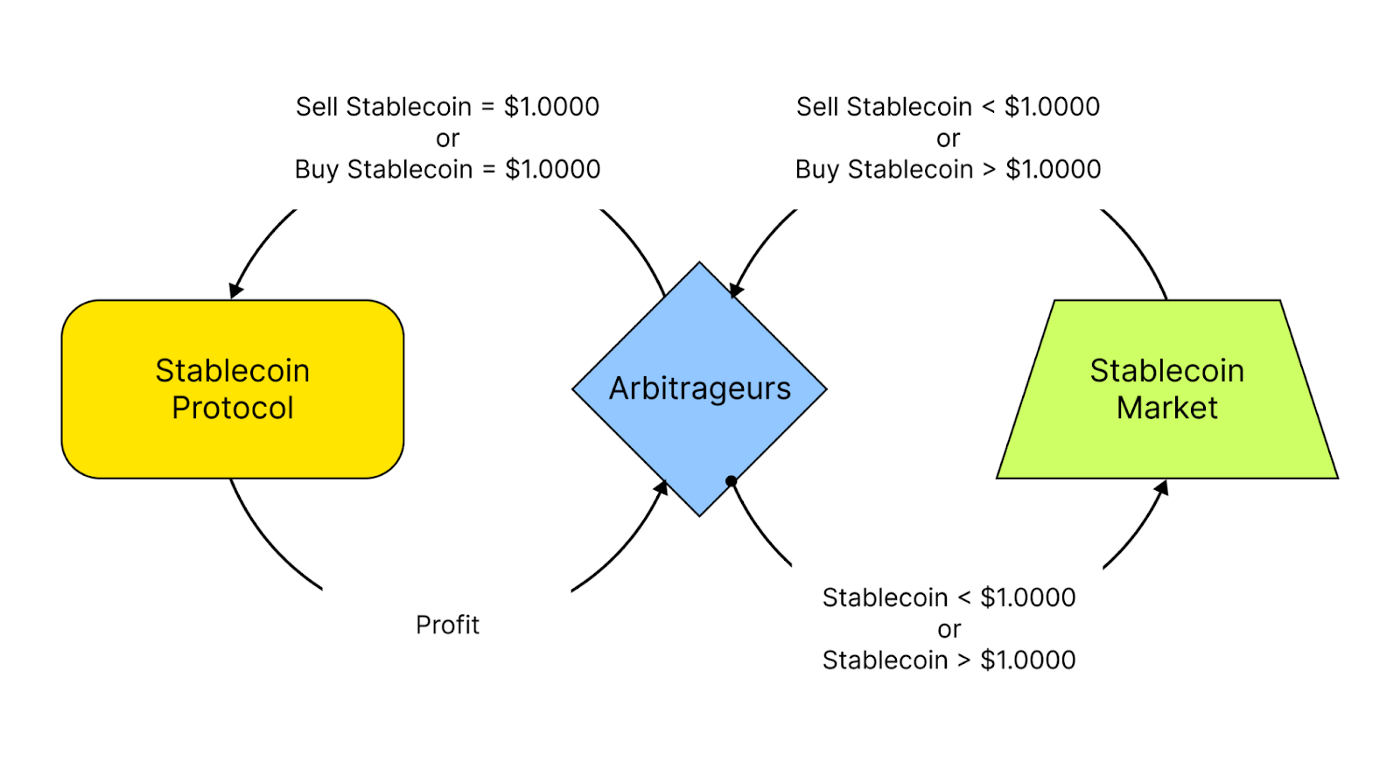

Finally, we have uncollateralized non-custodial stablecoins, sometimes known as “algorithmic” stablecoins. The design of these stablecoins is to address the centralization issues of custodial stablecoins. Also, the design eliminates the need for over-collateralization as with collateralized non-custodial stablecoins. As such, uncollateralized non-custodial stablecoins operate within an underlying digital or physical asset. Instead, it uses the basic economics of a supply and demand curve intertwined with cryptography, mathematics, and computer science.

Algorithmic stablecoins rely on smart contracts (or individuals called arbitrageurs) to inflate or reduce the circulating supply of stablecoins. An uncollateralized non-custodial stablecoin protocol will use an oracle to track the trading price of a stablecoin across different crypto exchanges. Let’s say an uncollateralized non-custodial stablecoin is tracking the price of $1. If the stablecoin rises above $1, the protocol will mint new stablecoins into circulation to inflate the supply. Thus, reducing its value. Conversely, if a stablecoin price fell below $1, the protocol would contract the supply, increasing the demand and, therefore, value.

As with any cryptocurrency project, using uncollateralized non-custodial stablecoins comes with risks. For example, smart contracts could contain bugs leaving platforms vulnerable to hacking. Additionally, algorithmic stablecoins run the risk of failing to maintain their price peg due to oracle failure or exploitation. The most recent algorithmic stablecoin project to collapse, reaching mainstream media headlines in the process, is Luna’s TerraUSD.

TerraUSD Collapse Overview

Once a top-ten leading blockchain project, the TerraUSD (UST) stablecoin deviated from its $1 peg, dropping to $0.22 on May 11, 2022, with cataclysmic results. As an algorithmic stablecoin, UST operated with its sister asset, LUNA, to maintain the price stability of $1. Alongside this, LUNA operates a multi-utility asset native to the Terra blockchain.

Essentially, traders could profit from arbitrage opportunities if UST swayed from its price peg. The basic algorithm was to ensure users could always exchange $1 of LUNA for $1 UST and vice versa. Users could buy UST at either above or below market price and then trade against the LUNA asset. In turn, this would put relative pressure on the UST price to restabilize at a $1 value.

Unfortunately, large sales resulted in a significant deviation from UST’s $1 peg, with the re-stabilizing algorithm failing to re-establish its equilibrium. As a result, traders began quickly selling their assets, causing immense downward price pressure on both LUNA and UST. Further, the algorithm truly began to fail when investors started existing their UST holdings at less than $1. On top of this, the dual-tokenomic design means that LUNA’s token supply has been heavily inflated since the sell-off of the UST stablecoin. LUNA’s all-time high of $116 is deemed unrealizable, with the asset trading falling to a low of $0.00014. At the time of writing, the newly-named Terra Luna Classic (LUNC) is trading at around $0.000106.

For readers who would like guidance on investing in crypto for the first time, see our Crypto For Beginners course at Moralis Academy. Here, students learn how to create an exchange account, buy crypto, and safely store assets offline. Discover the world-leading Web3 development and education suite today at Moralis Academy!

USD Coin (USDC) Collapse Rumors

Launched in 2018, USD Coin (USDC) is a custodial stablecoin run by Centre, an organization formed by Circle and Coinbase. Since its launch, the leading stablecoin project has surprised many investors with the rapid growth of its balance sheet. Recently, the centralized stablecoin project grabbed media attention after a Twitter user claimed a USDC collapse was on the cards. Specifically, crypto trader, Geralt Davidson, tweeted, fearing a UDSC collapse if Circles defaults on their reserves after losing money. Further, the narrative of a USDC collapse left fears about the future of stablecoins and the cryptocurrency as a whole.

However, Circle CEO Jeremy Allaire was quick to counteract these concerns. Circle published a statement regarding the tweet, assuring its users that USDC will always maintain a full 1:1 exchange with the US dollar. Moreover, Circle reminded the crypto market of its regulatory compliance with annual audits via the US State Money Transmission. Plus, USDC is fully compliant with the Financial Crimes Enforcement Network (FinCEN). The leading custodial stablecoin project linked users to its blog post, offering insights into collateral reports. As per Circle’s blog on USDC’s stability, transparency, and trust, the post reveals the following:

“As of 12:00pm EST Friday, May 13, 2022, the USDC reserve consisted of $11.6 billion cash (22.9%), $39.0 billion U.S. Treasuries (77.1%), for a total of $50.6 billion (100%), and there were 50.6 billion USDC in circulation,”.

Following clarification on the project’s validity and compliance, rumors of a USDC collapse have since subsided.

The Future of Stablecoins and Regulation

The collapse of a top-ten blockchain network coupled with rumors of other leading stablecoin projects in hot water yields much uncertainty around the future of stablecoins. However, there is a consensus across the community and governments that in order for the future of stablecoins to be sustainable, this will include the need for regulatory or legislative proposals. This will possibly include enforcement actions too. Following the downfall of TerraUSD, the US Treasury Secretary, Janet Yellen, states the demand for a legislative call-to-action. Notably, there needs to be a regulatory risk-prevention framework to secure the future of stablecoins.

Additionally, a bipartisan “Responsible Financial Innovation Act” bill was presented earlier in June 2022, seeking regulations of “payment stablecoins”. Such assets were initially defined through the Stablecoin Transparency of Reserves and Uniform Safe Transactions Act (the “TRUST Act.”) legislative proposal in April, a few months prior. The TRUST Act would assist in the regulatory foundations for the future of stablecoins. As such, the proposal suggests three types of entities issuing payment stablecoins, each operating under US banking laws. Additionally, this would see the introduction of a new entity infrastructure, a “national limited payment stablecoin issuers.” As per the TRUST Act, any stablecoin issue will need to present quarterly reports from public accounting firms. This will verify and ensure ownership of underlying assets.

Finally, discussions around the future of stablecoins feature in President Biden’s executive order for the responsible development of digital assets. Accordingly, Biden called on the Commodity Futures Trading Commission (CFTC), the Consumer Financial Protection Bureau (CFPB), and the Federal Trade Commission (FTC) to collaborate on the future of stablecoin regulations and risk frameworks.

Exploring USDC Collapse Rumors and the Future of Stablecoins Summary

Following TerraUSD’s algorithmic failure and rumors of a USDC collapse, the future of stablecoins appears somewhat uncertain. However, the rumors surrounding a USDC collapse are indeed only rumors, with Circle’s CEO assuring the community of its legitimacy. Accordingly, Circle published accounts confirming ownership of 100% of USDC’s underlying collateral. This comes after another leading custodial stablecoin project, Tether (USDT), received charges from the Commodity Futures Trading Commission (CFTC). After allegations of Tether not fully backing the entire circulating supply, the stablecoin project paid a fine of $41 million.

Other types of stablecoins include non-custodial stablecoins. Plus, a non-custodial stablecoin can be subcategorized as collateralized or uncollateralized. The former requires users to deposit collateral and receive stablecoin assets in return. An industry-leading example of this operation is DAI, available through Ethereum’s MakerDAO application. Uncollateralized or “algorithmic” stablecoins counter the centralized nature of custodial stablecoins and the inconvenient need for collateralization. However, they are inherently riskier. With the collapse of the TerraUST price peg, thousands of investors made a loss, and the overall crypto market suffered. In summary, although the future of stablecoins is uncertain, it appears certain there will not be a USDC collapse due to defaulting on debt positions. Moreover, the need for regulatory legislation surrounding stablecoin use is becoming increasingly urgent.

To learn how to navigate stormy market conditions, read our “How to Invest During a Crypto Bear Market” article next! Or, to learn on a deeper level the reasons for market fluctuations, see our “Understanding Crypto Crashes” article. Alternatively, for readers considering a career in Web3, check out our NFT Coding community. Discover the best place to learn NFT and metaverse development today!