In this article, we are going to explore various ways of integrating blockchain for small businesses. We’ll discuss the benefits of blockchain to both businesses and consumers. Also, we evaluate some of the things small businesses should ideally consider before implementing blockchain technology into their existing business model. Finally, we’ll look at the best way for small business owners to take the first step towards employing blockchain within their business. However, before we dig in, let’s briefly look at how this cutting-edge technology works.

Blockchain Technology Fundamentals Recap

Before we dive deep into how blockchain can benefit small businesses, we’ll briefly recap what blockchain is and how it works. On an “atomic” level, blockchain exists as pieces of code flying through the ether, monitored, managed, and validated by a global network of computers called nodes. The revolutionary aspects of the technology include its solution to the double-spending problem (infamous among the computer scientist community). Also, blockchain is fully transparent with public block explorers, so anyone anywhere can check a transaction.

Another benefit of blockchain is the decentralization and immutability of transactions. Unlike centralized payments services vulnerable to covert manipulation, blockchain transactions are cryptographically secure and mathematically verifiable. Accordingly, once a transaction is complete, there is no way of adjusting it. Even if a bad actor were to attempt to do so, they couldn’t without the other nodes in the network noticing. Further, the financial design of blockchains means that it is more profitable to participate and support rather than attack the network. In addition, operating across an international network means there is no single point of failure.

The popularity of blockchain is growing due to its ability to improve the time and cost efficiencies surrounding transactions. Traditional payments services typically take five to seven days to clear, with inefficient communications between numerous parties. However, with blockchain, payments are peer-to-peer with no third-party intermediaries. As a result, transaction settlement takes seconds (or minutes at worst) instead of days. Plus, the fees are substantially lower than using legacy systems.

For a dive into the technicalities of blockchain networks, see our Blockchain & Bitcoin Fundamentals course! Learn about UTXOs, mining nodes, and the differences between soft forks and hard forks. Plus, students will gain a deeper understanding of the proof-of-work (PoW) consensus mechanism. Kickstart your blockchain education with Moralis Academy today!

Smart Contracts

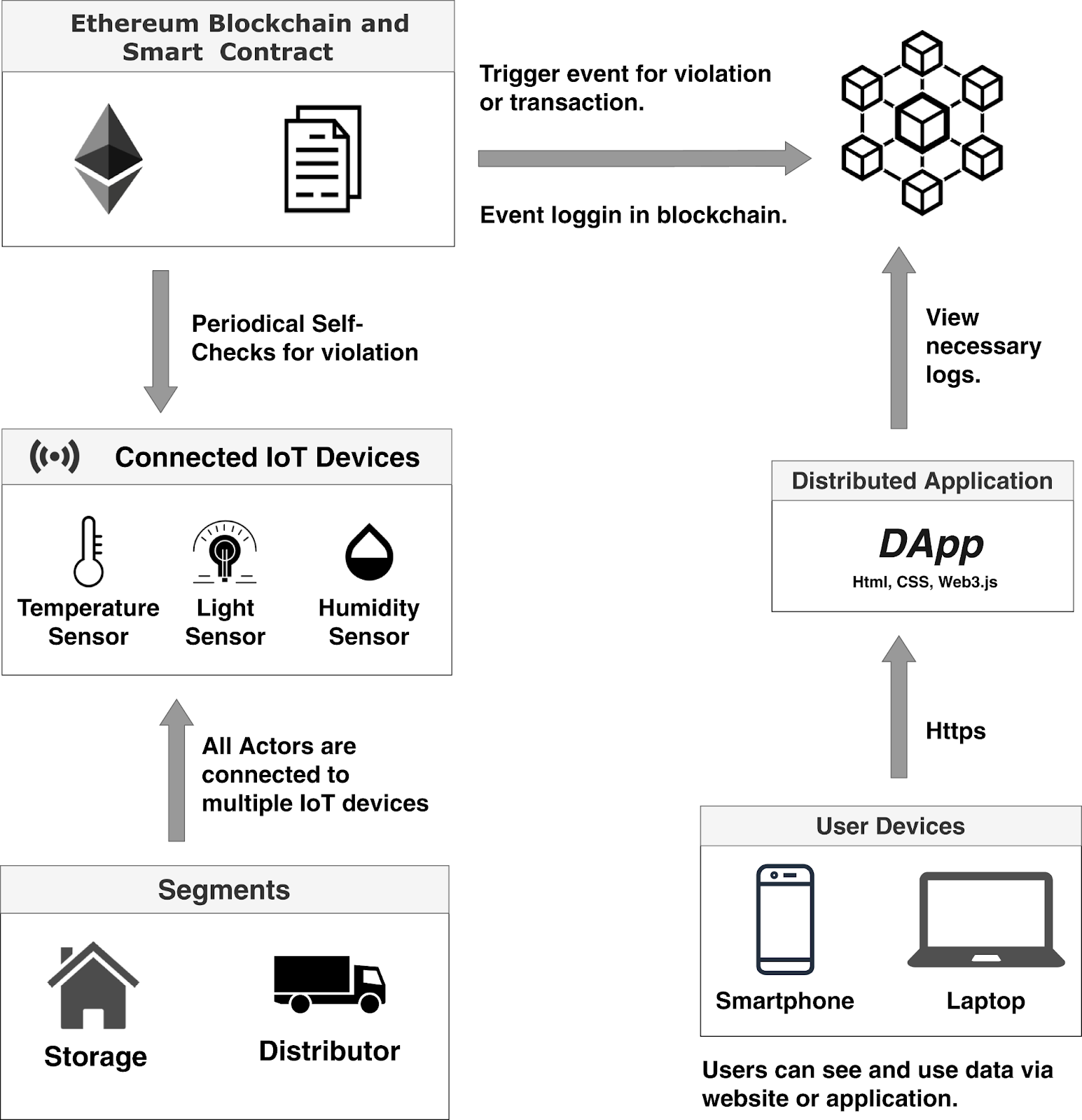

Bitcoin was the first blockchain to launch with the design of sending payment transactions between wallet A and wallet B. A few years later, the Ethereum blockchain launched, creating a decentralized blockchain landscape for developers to design, deploy, and manage decentralized applications (dapps). This is possible with the use of smart contracts. Smart contracts are pieces of code that many consider “programmable money”. In short, a smart contract can automate the execution of a transaction upon meeting a pre-set criterion, with the public and immutable functionalities of blockchain. For example, you could create a smart contract to motivate your kids in school. The smart contract could send $50 for every “A” and $30 for every “B” from your bank account to theirs. When the official results from the school publish, this could trigger the transaction with the respective amount.

Smart contracts are fundamental and critical to the operations of dapps. Plus, it’s not just payments that smart contracts can automate. Businesses can use smart contracts in conjunction with the internet of things (IoT) devices to automate orders, data transactions, and communications. For example, an IoT thermometer could communicate with a smart contract set up on a business’ blockchain network. The IoT device could monitor the temperature of goods en route from the manufacturer. If the temperature fell below the necessary temperature in transit, the IoT could alert the smart contract, triggering a “cancel order” for the spoiled goods. Simultaneously, a separate order could be placed for a new set of goods.

To discover how smart contracts work on a deeper level, be sure to check out the Ethereum Fundamentals course at Moralis Academy! You’ll learn the underlying differences between the two leading blockchains, Bitcoin and Ethereum, and about Ethereum Virtual Machine (EVM) and ERC-20 token standards.

How Small Businesses Can Benefit From Blockchain

There are several avenues one can consider when choosing to integrate blockchain for small businesses. The advantages of blockchain apply to business operations and communications to consumer-level end products or services. In addition, the technology can assist in public relations (PR) and marketing activities with novel forms of consumer engagement.

There are currently nearly 400 million small and medium enterprises (SMEs) globally, accounting for almost 70% of global employment. Any business that deals with money or transactions could benefit from integrating blockchain into existing IT infrastructure.

When considering blockchain for small businesses, the technology could ameliorate costly overheads and automate time-consuming activities. In addition, the security of transactions and data storage with blockchain far exceeds that of any traditional service. As such, blockchain can assist business owners with time and money-saving activities that save a failing business model.

Improve CMS and Workflow Efficiencies

From a business standpoint, blockchain could drastically optimize a company’s content management system (CMS). The transparency and immutability of the technology improve fact-checking and news validation alongside combating disinformation. Also, blockchain can scrap the need for timely and costly digital signatures certifying the authenticity of information. Instead, the confidence in authorship is transparent, with data integrity assured by computer science and mathematical proofs. In addition, smart contracts can assist in automating and tracking royalties, content, and digital rights.

Improving the quality of content will enhance the engagement and reputation of a business’ website. As a result, this can lead to higher conversion rates and, in turn, revenue.

Accounting

No matter how big or small, every business should have an accountant. The end-of-year number crunch each tax year is synonymous with high levels of stress and a race to find receipts and balance the books. However, blockchain for small businesses (and medium and large businesses alike) can substantially improve the overall accounting experience.

Transactions on a blockchain network go through extensive validation from the entire network of nodes prior to confirmation of the transaction on the chain. As a result, every transaction that is confirmed on the blockchain is mathematically verifiable as true. Therefore, this removes the need for the auditing process to establish validity in a business’ transactions. Running operations with a built-in transactions auditing software is another benefit of blockchain for small businesses. In addition, the transparency and traceability of blockchain make it easy to follow the movement of funds before and after a customer interacts with the business.

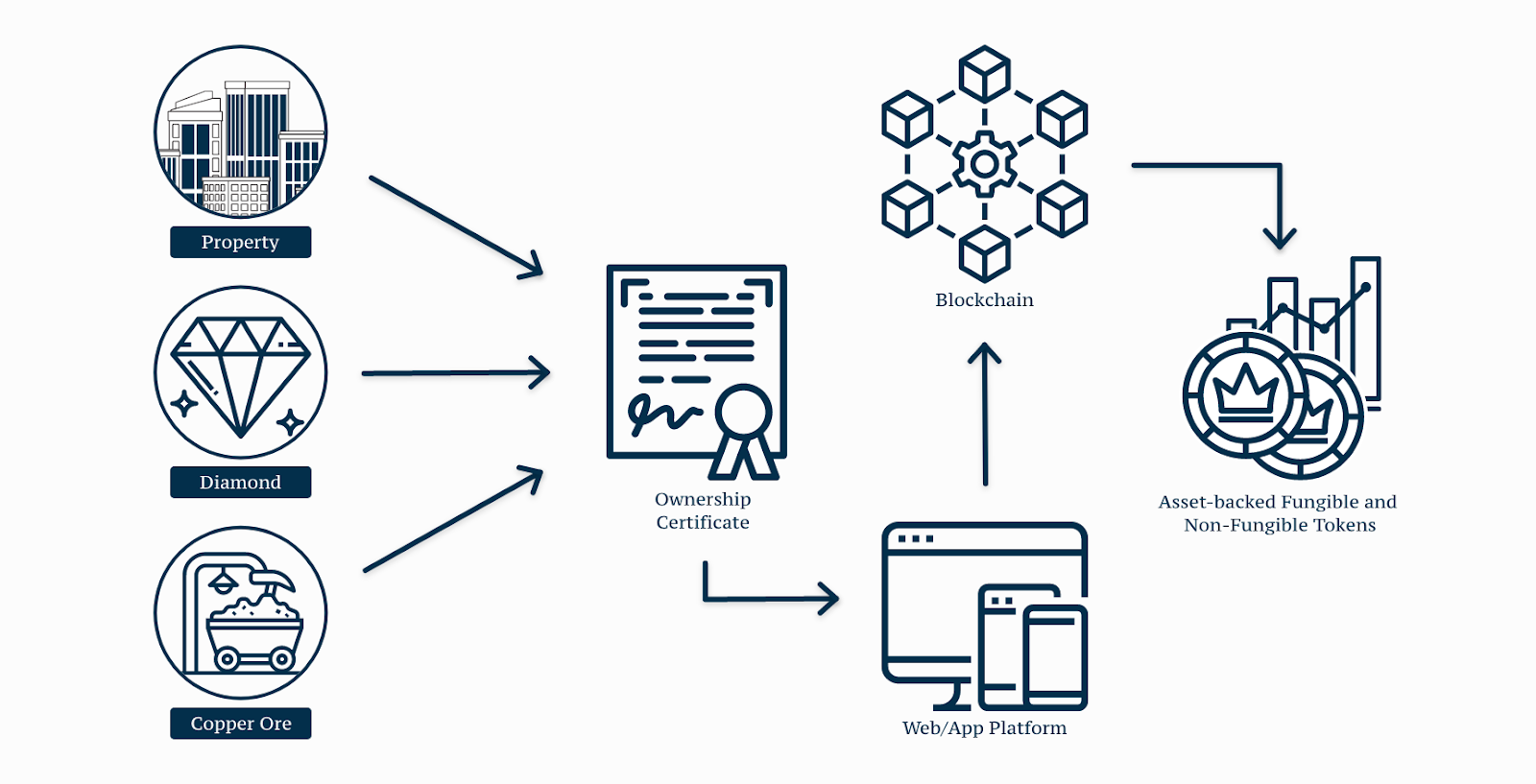

Tokenization

In addition to accounting and financial auditing, another advantage of blockchain for small businesses is the ability for tokenization. With the emergence of blockchain came digital cryptographic assets using various token standards, which can be broadly categorized into two types: fungible and non-fungible tokens (NFTs). Fungible tokens are interchangeable cryptocurrencies where every asset is worth the same. Conversely, NFTs are unique representations of digital or physical real-world assets.

Small businesses could integrate NFTs in primarily two ways. First, a business could tokenize its goods. This means businesses would know exactly where a product has been, for how long, and the environmental conditions of where it was made. As such, this could assist in more ethically oriented business decision-making. In addition, businesses could tokenize their goods or services for their consumers or end-users to register on the blockchain. This adds a novel avenue for engagement and interaction with customers alongside potential marketing activities.

Global Networking Opportunities

At the time of writing, the blockchain industry is still very niche. That said, there is rapid development and innovation in decentralized technologies, with the evolution of Web3 being one of the fastest-growing industries. A benefit of integrating blockchain for small businesses now is the forward-thinking and cutting-edge reputation it is likely to attract. Further, an increase in consumers could increase the opportunity for business-to-business (B2B) networking.

Blockchain is a decentralized technology run “by the people for the people”. The technology is borderless and permissionless, meaning there are no gatekeepers for international transactions. Introducing blockchain for small businesses creates a new, decentralized network of like-minded enterprising individuals. Particularly as the industry is still young, integrating blockchain could be a profitable move for garnering a credible reputation in the future. Moreover, accepting cryptocurrency as a form of payment (akin to ApplePay or PayPal) opens up new potential revenue avenues from an international market.

Considerations for Integrating Blockchain for Small Businesses

There are many benefits to implementing blockchain for small businesses, but there are some considerations too. First, if you’re planning on incorporating or accepting cryptocurrencies into a business model, be sure to check the legalities of doing so within your local jurisdiction. Each country and government maintain its own view surrounding the legalities of interacting with crypto assets. If you’re a small business considering accepting cryptocurrencies, seek local legal advice regarding any regulatory requirements.

Another consideration for integrating blockchain for small businesses is the development cost. Blockchain developers are specialist skill workers in extremely high demand and don’t come cheap. Be sure to budget accordingly and calculate the income saved on improved workflow efficiencies against the expenditure of hiring a blockchain developer.

Blockchain can assist in the accountability, transparency, and scalability of a business, large or small. For maximum profitability of implementing blockchain for small businesses, critically research and evaluate a long-term strategy. It may not be a profitable move to incorporate aspects of blockchain and decentralization just because it’s a trending activity to do so.

How to Start Implementing Blockchain for Small Businesses

If you’re a small business owner hoping to somehow integrate blockchain into your existing model, look no further. The first step in introducing blockchain for small businesses is educating the business owners, managers, and directors about blockchain basics and the benefits of decentralization. Our Blockchain Business Masterclass course is designed to give non-programmers an understanding of how centralized IT infrastructures work and how blockchain can improve this. Also, students learn how to integrate aspects of decentralization into existing IT systems!

Alternatively, our free Moralis Academy and Moralis blogs are full of educational content about the fundamentals and benefits of Web3 projects, technologies, industry updates, and more!

To discover many of the reasons why individuals and businesses alike are turning to blockchain, see our “Why to Learn Web3 Development” article. Understanding how blockchain works on a basic level puts you and your business at an advantage. Plus, it could save you valuable time and money by not outsourcing this knowledge from elsewhere. No matter your experience, expertise, or starting point, Moralis Academy can get you started safely on your blockchain journey today!

Exploring Blockchain for Small Businesses – Summary

Blockchain technology is a form of distributed ledger technology (DLT) that mathematically verifies transactions across a community of nodes. The technology is transparent and immutable, with 24/7 uptime and no single point of failure. As a result, blockchain can offer many benefits to businesses. When specifically evaluating the use of blockchain for small businesses, the technology can optimize workflows and increase operational and communication efficiencies. This could reduce the overheads needed for a small-scale business to survive turbulent market conditions. Moreover, the novelty and forward-thinking factor of implementing blockchain for consumer benefits could boost the reputation of a small business. Also, accepting cryptocurrencies means small businesses can expand their market potential to previously inaccessible international demographics.

There are many benefits of introducing blockchain for small businesses. However, it is worth first researching and gaining an understanding of the technology and its potential. This includes understanding how the technology works, various available options, and researching the legalities of introducing or accepting cryptocurrencies. With this knowledge, small businesses can strategize a long-term plan for integrating or scaling a business with blockchain. The best time to start will always be now! So, why not check out other topics on our blog to learn about the differences between some of the leading blockchain projects? If interested, start with our “Polkadot vs Cardano” article. Or, learn about one of the biggest social NFT clubs with our “Exploring ApeCoin (APE)” article!